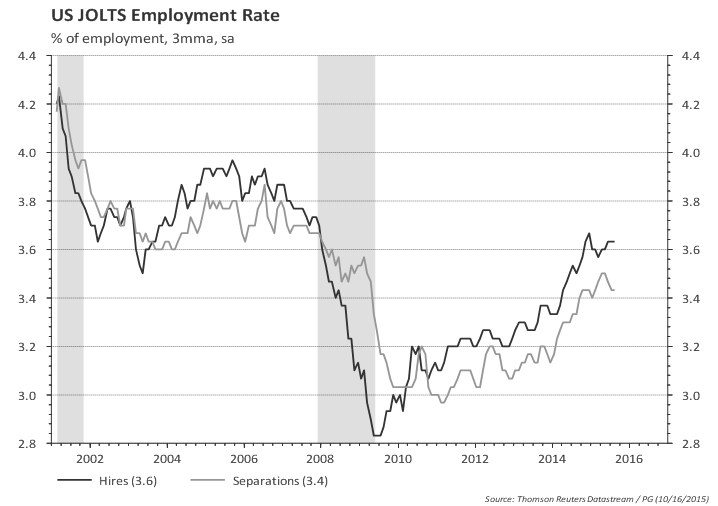

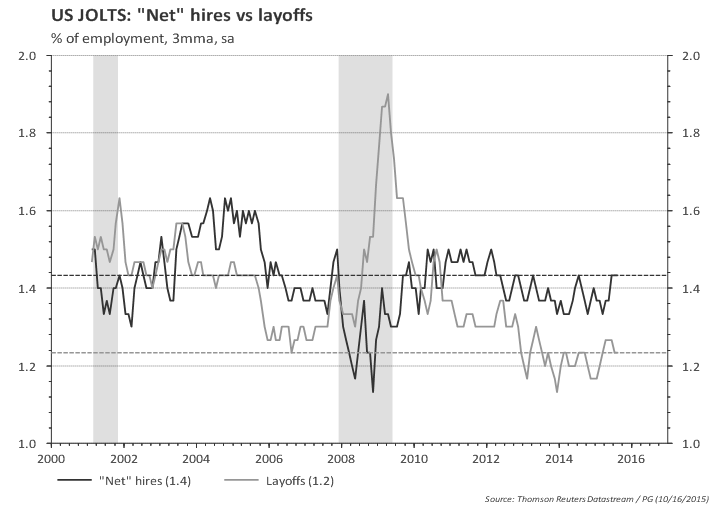

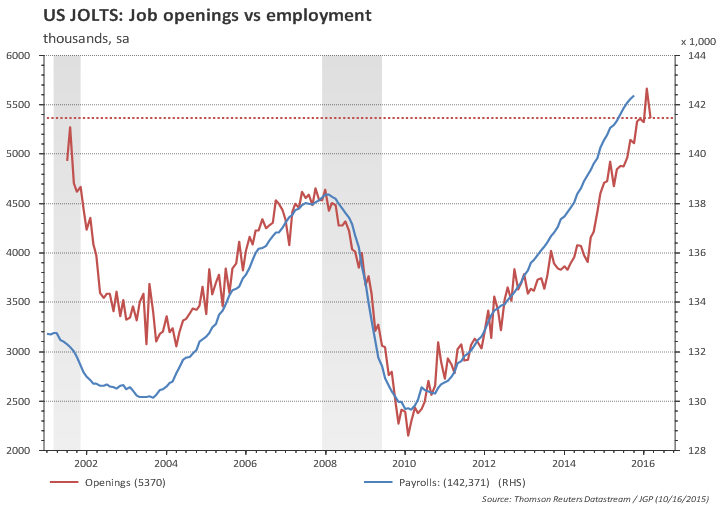

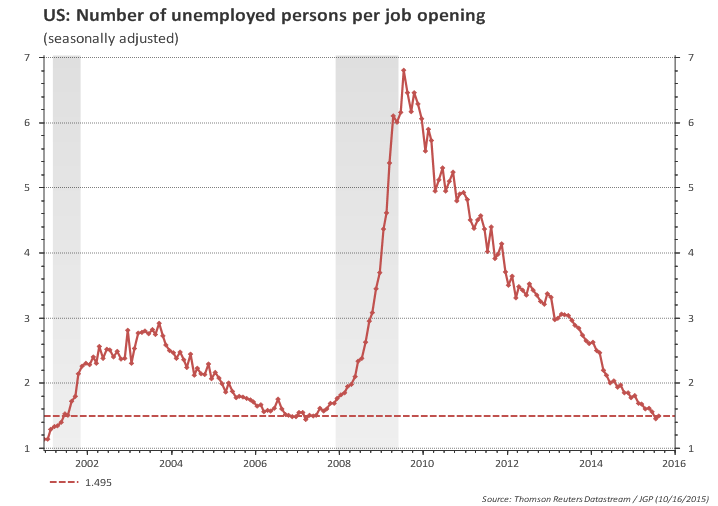

Main takeaways:

- Net job creation slowed down, as suggested by a mix of labor market data ('labor market conditions').

- Monthly payroll changed from being 'surprisingly resilient' to being 'disappointing'.

- While one should have expected the pace of job creation to slowdown, April's result can be traced back to 'construction', 'retail sales' and 'government' categories.

- Looking at the overall trend in those categories, one would hardly be too worried abut the weak prints in April.

- Also, hours worked and average hourly earnings posted healthy gains in April.

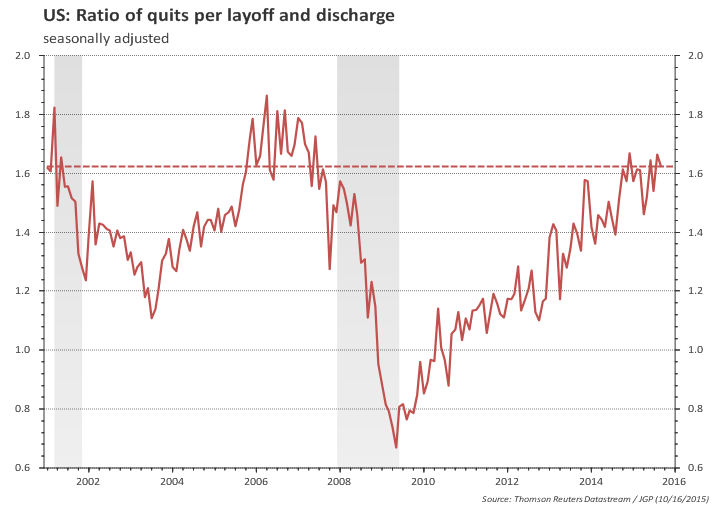

- Wage growth has steadily increased since early 2015; the Phillips curve seems to be alive and well.

- The household survey showed a 316 thousands loss of jobs in April; but this was on the back of an average gain of 464 thousands in the first quarter.

- Despite the loss of jobs, unemployment rate remained stable at 5% since participation rate gave back part of the previous gains (from 63% to 62.8%).

Most people were surprised job creation was very resilient to the tightening of financial conditions and the GDP slowdown.

Now, most people are disappointed by the slowdown in April's payroll...go figure!

Establishment Report

Net job creation in the private sector slowed from about 230k per month in the second half of 2015 to 183k/month in the first four months of 2016. This should not be a major surprise. Indeed, my own track of labor market conditions suggested "underlying private payroll running at around 170 / 183 thousands/month". (See "US Labor Market Conditions").

The chart below shows the evolution of the 6-month payroll average in real time. It shows an uptrend in the second half of 2015 that was at odds with the tightening of financial conditions observed in the same period.

To be fair, the reason for concern / disappointment is probably more linked to the fact that, when looking at divergent signs (employment pickup vs growth slowdown) some observers were putting more emphasis on the more upbeat employment date -- an emphasis that several Fed members often also give in their own speeches.

But specifically for April, we can trace the slowdown in private job creation to construction and retail sales. Construction added, on average, 36 thousand jobs per month in 4Q 15 / 1Q 16 and April reported a mere 1k increase. Similarly, retail sales added 40 thousands per month in 4Q/1Q and April printed minus 3k.

The following two charts plot the employment level in retail and construction, as well as the trend in the last two years and the last 12 months (orange bars show monthly changes). One can hardly see a problem in those employment groups.

|  |

Also, the weakness in the establishment report was confined to the headline payroll number, since both hours worked and wages increased in the month. Total hours worked rose a healthy 0.4% in April (for production workers) and now stand at 1.6% above the first quarter average level. This is not great, but compares favorable to the first quarter (1.2%) and to sub 2% GDP growth estimates for the second quarter.

Average hourly earnings also posted a strong 0.3% mom growth in April, leading to 2.5% growth compared to a year ago. But what is more striking, in my view, is that wage growth has steadily increased since early 2015 at the same time that most pundits complain that wages are not going anywhere. The chart below shows the Phillips curve seem to be well and alive: wage growth starts to increase following two years of very strong job growth (2014 and 2015) and with unemployment rate very close to NAIRU.

|  |

Total (nominal) labor income rose a strong 0.7% mom in April, but the carry over for the second quarter is a mere 3.3% for production workers and 3.7% for all employees. With rising inflation, this means real purchasing power is going down. Consumers would have to tap their (increasing) savings if consumption is expected to rebound from the weak first quarter.

Household Report

The household report is often very volatile in a monthly basis, but it painted a weaker picture with net job losses of 316 thousands in the month. Truth be told, the household report had shown an average gain of 464 thousands per month in the first quarter. Indeed, even with April's losses, the average 2016 employment gain in the household report stands at 270k/month.

Despite the losses in the month, unemployment rate remained flat at 5% due to a 362 thousand drop in the labor force. Participation rate dropped from 63% to 62.8% and remains close to the level observed in 2014 and early 2015. The pick-up in LFPR since last September has confused many observers and there is no clear reason why that has happened; contrary to often stated views, the pick up does not seem to be due to more people joining the labor force in response to a strong labor market. It is very difficult to have confidence in a short term forecast of LFPR but, over the years, demographics should dominate short-term fluctuations leading to lower participation in the coming years.

If one assumes labor participation remains flat at current levels, then a monthly job creation of 175k would lead to unemployment rate at 4.6% by the end of the year.

|  |

The charts below show employment to population ratio and the broader U6 unemployment rate.

|  |