Main takeaways:

- World trade volumes resilient, despite risk-off in financial markets.

- World trade volumes growing at around 1.8% per year, but with sharp contrast between advanced and emerging economies.

- Advanced economies imports growing at a strong pace, but growth might have slowed a bit in recent months.

- Trade volumes in emerging economies, on the other hand, are flat (but with some tentative sign of improvement in imports).

The Netherlands Bureau for Economic Analysis (CPB - Centraal Planbureau) has released world trade volume and industrial production data for January.

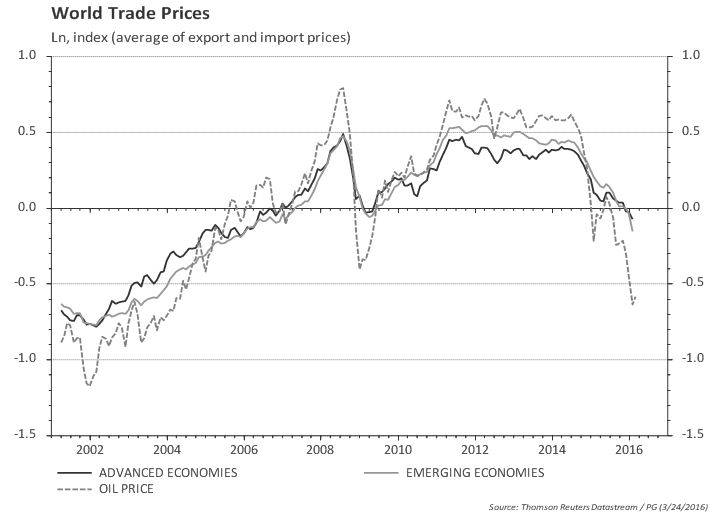

World trade prices (exports and imports) dropped materially since mid-2014, in tandem with oil prices. Trade prices fell by 45 % for advanced economies (AE), 60% for emerging economies, while oil prices dropped 120% in the same period ! (welcome to log % changes !!)

This has confused some pundits that often mention the collapse in global trade growth looking only at nominal (or current US$) trade performance. Looking at trade volumes one reaches a different conclusion (more on this below).

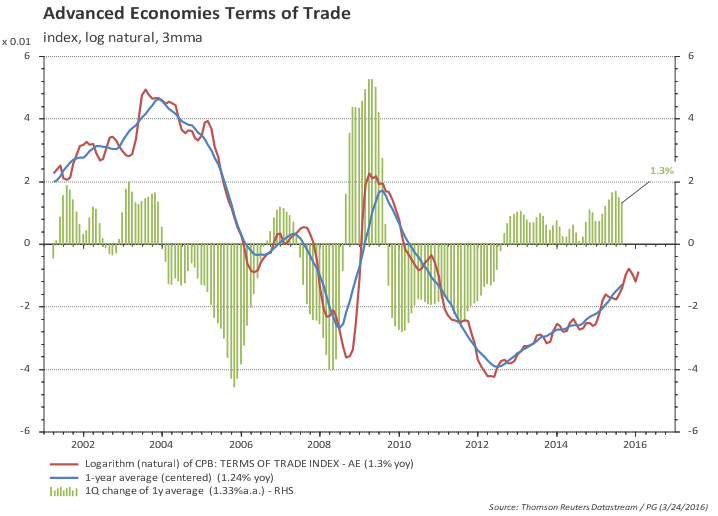

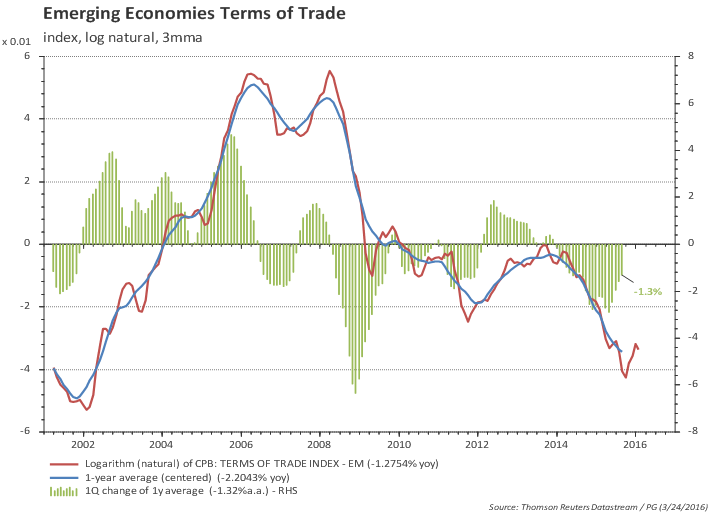

The overall drop in trade prices for both emerging and advanced economies masks an important difference: the regions faced opposite terms of trade shocks in recent years. Advanced economies are facing improving terms of trade, while EM economies are facing a declining terms of trade (but with a tentative sign of a rebound, see charts).

Advanced Economies

Looking at trade volumes, one can see that demand (imports) from advanced economies picked up late 2013 and is growing at a healthy 3.5% pace, but might have slowed a bit more recently.

|  |

Emerging Economies

Emerging economies show a completely different picture. Both export and import volumes have been relatively flat since mid-2014. More recently, imports are tentatively rebounding, but exports remain lackluster.

|  |

World

The consolidated world trade statistics show a puzzling divergence: consolidated imports (of which EM account for one-third) is growing at a healthy pace, while consolidated exports (of which EM account for 40%) are roughly flat. Growth of average trade volume is at 1% yoy, with imports growing at 2%yoy and exports flat.

|  |

|  |